출처 : http://a-little-book-of-r-for-time-series.readthedocs.io/en/latest/src/timeseries.html

Using R for Time Series Analysis

Time Series Analysis

This booklet itells you how to use the R statistical software to carry out some simple analyses that are common in analysing time series data.

This booklet assumes that the reader has some basic knowledge of time series analysis, and the principal focus of the booklet is not to explain time series analysis, but rather to explain how to carry out these analyses using R.

If you are new to time series analysis, and want to learn more about any of the concepts presented here, I would highly recommend the Open University book “Time series” (product code M249/02), available from from the Open University Shop.

In this booklet, I will be using time series data sets that have been kindly made available by Rob Hyndman in his Time Series Data Library at http://robjhyndman.com/TSDL/.

There is a pdf version of this booklet available at https://media.readthedocs.org/pdf/a-little-book-of-r-for-time-series/latest/a-little-book-of-r-for-time-series.pdf.

If you like this booklet, you may also like to check out my booklet on using R for biomedical statistics,http://a-little-book-of-r-for-biomedical-statistics.readthedocs.org/, and my booklet on using R for multivariate analysis, http://little-book-of-r-for-multivariate-analysis.readthedocs.org/.

Reading Time Series Data

The first thing that you will want to do to analyse your time series data will be to read it into R, and to plot the time series. You can read data into R using the scan() function, which assumes that your data for successive time points is in a simple text file with one column.

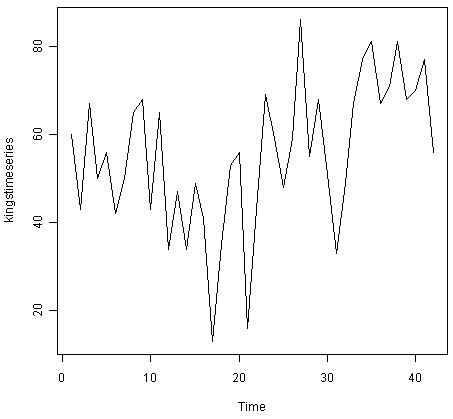

For example, the file http://robjhyndman.com/tsdldata/misc/kings.dat contains data on the age of death of successive kings of England, starting with William the Conqueror (original source: Hipel and Mcleod, 1994).

The data set looks like this:

Age of Death of Successive Kings of England #starting with William the Conqueror #Source: McNeill, "Interactive Data Analysis" 60 43 67 50 56 42 50 65 68 43 65 34 ...

Only the first few lines of the file have been shown. The first three lines contain some comment on the data, and we want to ignore this when we read the data into R. We can use this by using the “skip” parameter of the scan() function, which specifies how many lines at the top of the file to ignore. To read the file into R, ignoring the first three lines, we type:

> kings <- scan("http://robjhyndman.com/tsdldata/misc/kings.dat",skip=3) Read 42 items > kings [1] 60 43 67 50 56 42 50 65 68 43 65 34 47 34 49 41 13 35 53 56 16 43 69 59 48 [26] 59 86 55 68 51 33 49 67 77 81 67 71 81 68 70 77 56

In this case the age of death of 42 successive kings of England has been read into the variable ‘kings’.

Once you have read the time series data into R, the next step is to store the data in a time series object in R, so that you can use R’s many functions for analysing time series data. To store the data in a time series object, we use the ts() function in R. For example, to store the data in the variable ‘kings’ as a time series object in R, we type:

> kingstimeseries <- ts(kings) > kingstimeseries Time Series: Start = 1 End = 42 Frequency = 1 [1] 60 43 67 50 56 42 50 65 68 43 65 34 47 34 49 41 13 35 53 56 16 43 69 59 48 [26] 59 86 55 68 51 33 49 67 77 81 67 71 81 68 70 77 56

Sometimes the time series data set that you have may have been collected at regular intervals that were less than one year, for example, monthly or quarterly. In this case, you can specify the number of times that data was collected per year by using the ‘frequency’ parameter in the ts() function. For monthly time series data, you set frequency=12, while for quarterly time series data, you set frequency=4.

You can also specify the first year that the data was collected, and the first interval in that year by using the ‘start’ parameter in the ts() function. For example, if the first data point corresponds to the second quarter of 1986, you would set start=c(1986,2).

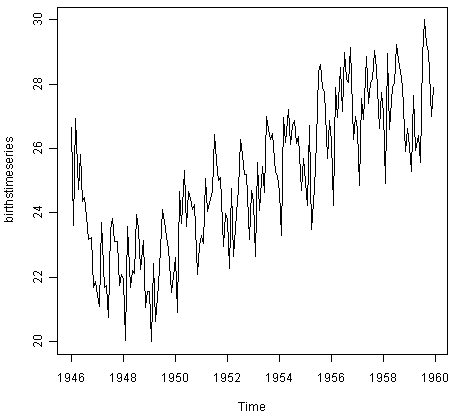

An example is a data set of the number of births per month in New York city, from January 1946 to December 1959 (originally collected by Newton). This data is available in the file http://robjhyndman.com/tsdldata/data/nybirths.dat We can read the data into R, and store it as a time series object, by typing:

> births <- scan("http://robjhyndman.com/tsdldata/data/nybirths.dat") Read 168 items > birthstimeseries <- ts(births, frequency=12, start=c(1946,1)) > birthstimeseries Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1946 26.663 23.598 26.931 24.740 25.806 24.364 24.477 23.901 23.175 23.227 21.672 21.870 1947 21.439 21.089 23.709 21.669 21.752 20.761 23.479 23.824 23.105 23.110 21.759 22.073 1948 21.937 20.035 23.590 21.672 22.222 22.123 23.950 23.504 22.238 23.142 21.059 21.573 1949 21.548 20.000 22.424 20.615 21.761 22.874 24.104 23.748 23.262 22.907 21.519 22.025 1950 22.604 20.894 24.677 23.673 25.320 23.583 24.671 24.454 24.122 24.252 22.084 22.991 1951 23.287 23.049 25.076 24.037 24.430 24.667 26.451 25.618 25.014 25.110 22.964 23.981 1952 23.798 22.270 24.775 22.646 23.988 24.737 26.276 25.816 25.210 25.199 23.162 24.707 1953 24.364 22.644 25.565 24.062 25.431 24.635 27.009 26.606 26.268 26.462 25.246 25.180 1954 24.657 23.304 26.982 26.199 27.210 26.122 26.706 26.878 26.152 26.379 24.712 25.688 1955 24.990 24.239 26.721 23.475 24.767 26.219 28.361 28.599 27.914 27.784 25.693 26.881 1956 26.217 24.218 27.914 26.975 28.527 27.139 28.982 28.169 28.056 29.136 26.291 26.987 1957 26.589 24.848 27.543 26.896 28.878 27.390 28.065 28.141 29.048 28.484 26.634 27.735 1958 27.132 24.924 28.963 26.589 27.931 28.009 29.229 28.759 28.405 27.945 25.912 26.619 1959 26.076 25.286 27.660 25.951 26.398 25.565 28.865 30.000 29.261 29.012 26.992 27.897

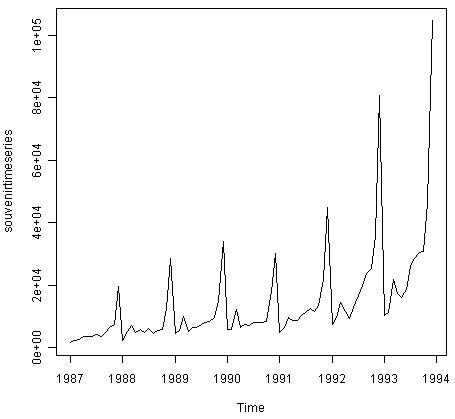

Similarly, the file http://robjhyndman.com/tsdldata/data/fancy.dat contains monthly sales for a souvenir shop at a beach resort town in Queensland, Australia, for January 1987-December 1993 (original data from Wheelwright and Hyndman, 1998). We can read the data into R by typing:

> souvenir <- scan("http://robjhyndman.com/tsdldata/data/fancy.dat") Read 84 items > souvenirtimeseries <- ts(souvenir, frequency=12, start=c(1987,1)) > souvenirtimeseries Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1987 1664.81 2397.53 2840.71 3547.29 3752.96 3714.74 4349.61 3566.34 5021.82 6423.48 7600.60 19756.21 1988 2499.81 5198.24 7225.14 4806.03 5900.88 4951.34 6179.12 4752.15 5496.43 5835.10 12600.08 28541.72 1989 4717.02 5702.63 9957.58 5304.78 6492.43 6630.80 7349.62 8176.62 8573.17 9690.50 15151.84 34061.01 1990 5921.10 5814.58 12421.25 6369.77 7609.12 7224.75 8121.22 7979.25 8093.06 8476.70 17914.66 30114.41 1991 4826.64 6470.23 9638.77 8821.17 8722.37 10209.48 11276.55 12552.22 11637.39 13606.89 21822.11 45060.69 1992 7615.03 9849.69 14558.40 11587.33 9332.56 13082.09 16732.78 19888.61 23933.38 25391.35 36024.80 80721.71 1993 10243.24 11266.88 21826.84 17357.33 15997.79 18601.53 26155.15 28586.52 30505.41 30821.33 46634.38 104660.67

Plotting Time Series

Once you have read a time series into R, the next step is usually to make a plot of the time series data, which you can do with the plot.ts() function in R.

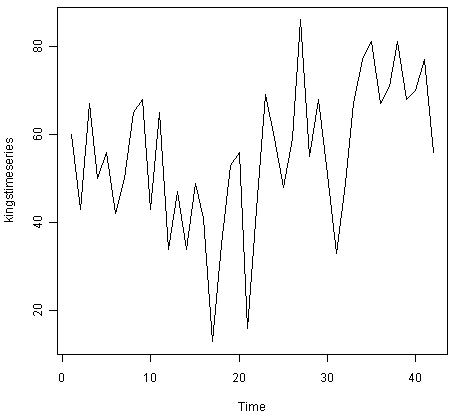

For example, to plot the time series of the age of death of 42 successive kings of England, we type:

> plot.ts(kingstimeseries)

We can see from the time plot that this time series could probably be described using an additive model, since the random fluctuations in the data are roughly constant in size over time.

Likewise, to plot the time series of the number of births per month in New York city, we type:

> plot.ts(birthstimeseries)

We can see from this time series that there seems to be seasonal variation in the number of births per month: there is a peak every summer, and a trough every winter. Again, it seems that this time series could probably be described using an additive model, as the seasonal fluctuations are roughly constant in size over time and do not seem to depend on the level of the time series, and the random fluctuations also seem to be roughly constant in size over time.

Similarly, to plot the time series of the monthly sales for the souvenir shop at a beach resort town in Queensland, Australia, we type:

> plot.ts(souvenirtimeseries)

In this case, it appears that an additive model is not appropriate for describing this time series, since the size of the seasonal fluctuations and random fluctuations seem to increase with the level of the time series. Thus, we may need to transform the time series in order to get a transformed time series that can be described using an additive model. For example, we can transform the time series by calculating the natural log of the original data:

> logsouvenirtimeseries <- log(souvenirtimeseries) > plot.ts(logsouvenirtimeseries)

Here we can see that the size of the seasonal fluctuations and random fluctuations in the log-transformed time series seem to be roughly constant over time, and do not depend on the level of the time series. Thus, the log-transformed time series can probably be described using an additive model.

Decomposing Time Series

Decomposing a time series means separating it into its constituent components, which are usually a trend component and an irregular component, and if it is a seasonal time series, a seasonal component.

Decomposing Non-Seasonal Data

A non-seasonal time series consists of a trend component and an irregular component. Decomposing the time series involves trying to separate the time series into these components, that is, estimating the the trend component and the irregular component.

To estimate the trend component of a non-seasonal time series that can be described using an additive model, it is common to use a smoothing method, such as calculating the simple moving average of the time series.

The SMA() function in the “TTR” R package can be used to smooth time series data using a simple moving average. To use this function, we first need to install the “TTR” R package (for instructions on how to install an R package, see How to install an R package). Once you have installed the “TTR” R package, you can load the “TTR” R package by typing:

> library("TTR")

You can then use the “SMA()” function to smooth time series data. To use the SMA() function, you need to specify the order (span) of the simple moving average, using the parameter “n”. For example, to calculate a simple moving average of order 5, we set n=5 in the SMA() function.

For example, as discussed above, the time series of the age of death of 42 successive kings of England appears is non-seasonal, and can probably be described using an additive model, since the random fluctuations in the data are roughly constant in size over time:

Thus, we can try to estimate the trend component of this time series by smoothing using a simple moving average. To smooth the time series using a simple moving average of order 3, and plot the smoothed time series data, we type:

> kingstimeseriesSMA3 <- SMA(kingstimeseries,n=3) > plot.ts(kingstimeseriesSMA3)

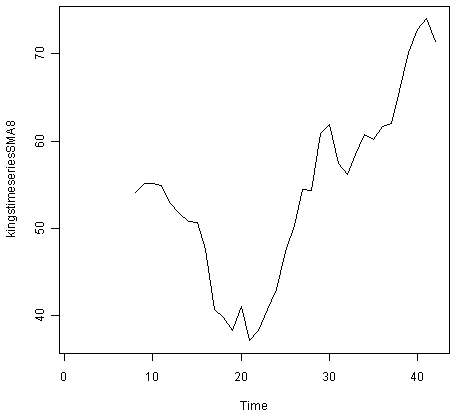

There still appears to be quite a lot of random fluctuations in the time series smoothed using a simple moving average of order 3. Thus, to estimate the trend component more accurately, we might want to try smoothing the data with a simple moving average of a higher order. This takes a little bit of trial-and-error, to find the right amount of smoothing. For example, we can try using a simple moving average of order 8:

> kingstimeseriesSMA8 <- SMA(kingstimeseries,n=8) > plot.ts(kingstimeseriesSMA8)

The data smoothed with a simple moving average of order 8 gives a clearer picture of the trend component, and we can see that the age of death of the English kings seems to have decreased from about 55 years old to about 38 years old during the reign of the first 20 kings, and then increased after that to about 73 years old by the end of the reign of the 40th king in the time series.

Decomposing Seasonal Data

A seasonal time series consists of a trend component, a seasonal component and an irregular component. Decomposing the time series means separating the time series into these three components: that is, estimating these three components.

To estimate the trend component and seasonal component of a seasonal time series that can be described using an additive model, we can use the “decompose()” function in R. This function estimates the trend, seasonal, and irregular components of a time series that can be described using an additive model.

The function “decompose()” returns a list object as its result, where the estimates of the seasonal component, trend component and irregular component are stored in named elements of that list objects, called “seasonal”, “trend”, and “random” respectively.

For example, as discussed above, the time series of the number of births per month in New York city is seasonal with a peak every summer and trough every winter, and can probably be described using an additive model since the seasonal and random fluctuations seem to be roughly constant in size over time:

To estimate the trend, seasonal and irregular components of this time series, we type:

> birthstimeseriescomponents <- decompose(birthstimeseries)

The estimated values of the seasonal, trend and irregular components are now stored in variables birthstimeseriescomponents$seasonal, birthstimeseriescomponents$trend and birthstimeseriescomponents$random. For example, we can print out the estimated values of the seasonal component by typing:

> birthstimeseriescomponents$seasonal # get the estimated values of the seasonal component Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1946 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1947 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1948 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1949 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1950 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1951 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1952 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1953 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1954 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1955 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1956 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1957 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1958 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197 1959 -0.6771947 -2.0829607 0.8625232 -0.8016787 0.2516514 -0.1532556 1.4560457 1.1645938 0.6916162 0.7752444 -1.1097652 -0.3768197

The estimated seasonal factors are given for the months January-December, and are the same for each year. The largest seasonal factor is for July (about 1.46), and the lowest is for February (about -2.08), indicating that there seems to be a peak in births in July and a trough in births in February each year.

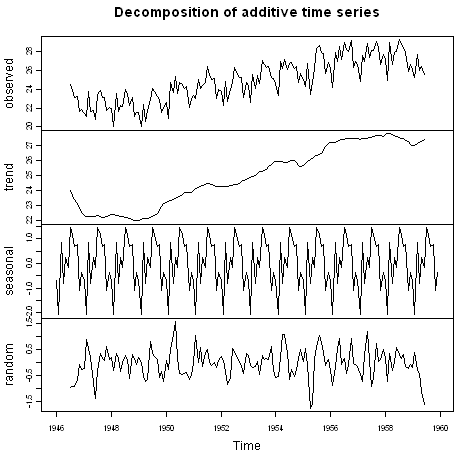

We can plot the estimated trend, seasonal, and irregular components of the time series by using the “plot()” function, for example:

> plot(birthstimeseriescomponents)

The plot above shows the original time series (top), the estimated trend component (second from top), the estimated seasonal component (third from top), and the estimated irregular component (bottom). We see that the estimated trend component shows a small decrease from about 24 in 1947 to about 22 in 1948, followed by a steady increase from then on to about 27 in 1959.

Seasonally Adjusting

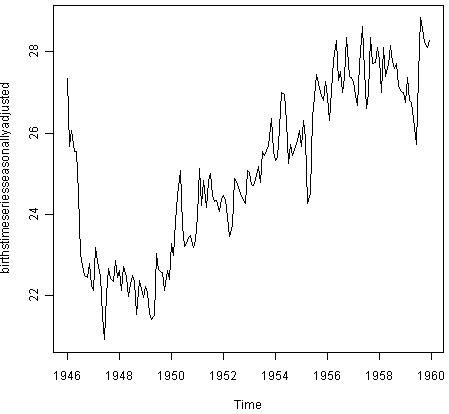

If you have a seasonal time series that can be described using an additive model, you can seasonally adjust the time series by estimating the seasonal component, and subtracting the estimated seasonal component from the original time series. We can do this using the estimate of the seasonal component calculated by the “decompose()” function.

For example, to seasonally adjust the time series of the number of births per month in New York city, we can estimate the seasonal component using “decompose()”, and then subtract the seasonal component from the original time series:

> birthstimeseriescomponents <- decompose(birthstimeseries) > birthstimeseriesseasonallyadjusted <- birthstimeseries - birthstimeseriescomponents$seasonal

We can then plot the seasonally adjusted time series using the “plot()” function, by typing:

> plot(birthstimeseriesseasonallyadjusted)

You can see that the seasonal variation has been removed from the seasonally adjusted time series. The seasonally adjusted time series now just contains the trend component and an irregular component.

Forecasts using Exponential Smoothing

Exponential smoothing can be used to make short-term forecasts for time series data.

Simple Exponential Smoothing

If you have a time series that can be described using an additive model with constant level and no seasonality, you can use simple exponential smoothing to make short-term forecasts.

The simple exponential smoothing method provides a way of estimating the level at the current time point. Smoothing is controlled by the parameter alpha; for the estimate of the level at the current time point. The value of alpha; lies between 0 and 1. Values of alpha that are close to 0 mean that little weight is placed on the most recent observations when making forecasts of future values.

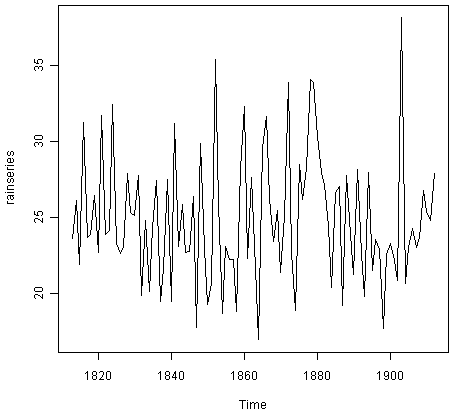

For example, the file http://robjhyndman.com/tsdldata/hurst/precip1.dat contains total annual rainfall in inches for London, from 1813-1912 (original data from Hipel and McLeod, 1994). We can read the data into R and plot it by typing:

> rain <- scan("http://robjhyndman.com/tsdldata/hurst/precip1.dat",skip=1) Read 100 items > rainseries <- ts(rain,start=c(1813)) > plot.ts(rainseries)

You can see from the plot that there is roughly constant level (the mean stays constant at about 25 inches). The random fluctuations in the time series seem to be roughly constant in size over time, so it is probably appropriate to describe the data using an additive model. Thus, we can make forecasts using simple exponential smoothing.

To make forecasts using simple exponential smoothing in R, we can fit a simple exponential smoothing predictive model using the “HoltWinters()” function in R. To use HoltWinters() for simple exponential smoothing, we need to set the parameters beta=FALSE and gamma=FALSE in the HoltWinters() function (the beta and gamma parameters are used for Holt’s exponential smoothing, or Holt-Winters exponential smoothing, as described below).

The HoltWinters() function returns a list variable, that contains several named elements.

For example, to use simple exponential smoothing to make forecasts for the time series of annual rainfall in London, we type:

> rainseriesforecasts <- HoltWinters(rainseries, beta=FALSE, gamma=FALSE) > rainseriesforecasts Smoothing parameters: alpha: 0.02412151 beta : FALSE gamma: FALSE Coefficients: [,1] a 24.67819

The output of HoltWinters() tells us that the estimated value of the alpha parameter is about 0.024. This is very close to zero, telling us that the forecasts are based on both recent and less recent observations (although somewhat more weight is placed on recent observations).

By default, HoltWinters() just makes forecasts for the same time period covered by our original time series. In this case, our original time series included rainfall for London from 1813-1912, so the forecasts are also for 1813-1912.

In the example above, we have stored the output of the HoltWinters() function in the list variable “rainseriesforecasts”. The forecasts made by HoltWinters() are stored in a named element of this list variable called “fitted”, so we can get their values by typing:

> rainseriesforecasts$fitted Time Series: Start = 1814 End = 1912 Frequency = 1 xhat level 1814 23.56000 23.56000 1815 23.62054 23.62054 1816 23.57808 23.57808 1817 23.76290 23.76290 1818 23.76017 23.76017 1819 23.76306 23.76306 1820 23.82691 23.82691 ... 1905 24.62852 24.62852 1906 24.58852 24.58852 1907 24.58059 24.58059 1908 24.54271 24.54271 1909 24.52166 24.52166 1910 24.57541 24.57541 1911 24.59433 24.59433 1912 24.59905 24.59905

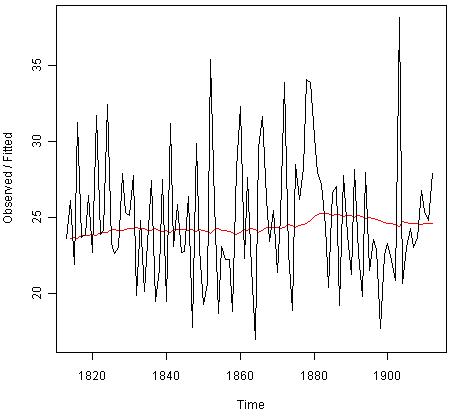

We can plot the original time series against the forecasts by typing:

> plot(rainseriesforecasts)

The plot shows the original time series in black, and the forecasts as a red line. The time series of forecasts is much smoother than the time series of the original data here.

As a measure of the accuracy of the forecasts, we can calculate the sum of squared errors for the in-sample forecast errors, that is, the forecast errors for the time period covered by our original time series. The sum-of-squared-errors is stored in a named element of the list variable “rainseriesforecasts” called “SSE”, so we can get its value by typing:

> rainseriesforecasts$SSE [1] 1828.855

That is, here the sum-of-squared-errors is 1828.855.

It is common in simple exponential smoothing to use the first value in the time series as the initial value for the level. For example, in the time series for rainfall in London, the first value is 23.56 (inches) for rainfall in 1813. You can specify the initial value for the level in the HoltWinters() function by using the “l.start” parameter. For example, to make forecasts with the initial value of the level set to 23.56, we type:

> HoltWinters(rainseries, beta=FALSE, gamma=FALSE, l.start=23.56)

As explained above, by default HoltWinters() just makes forecasts for the time period covered by the original data, which is 1813-1912 for the rainfall time series. We can make forecasts for further time points by using the “forecast.HoltWinters()” function in the R “forecast” package. To use the forecast.HoltWinters() function, we first need to install the “forecast” R package (for instructions on how to install an R package, see How to install an R package).

Once you have installed the “forecast” R package, you can load the “forecast” R package by typing:

> library("forecast")

When using the forecast.HoltWinters() function, as its first argument (input), you pass it the predictive model that you have already fitted using the HoltWinters() function. For example, in the case of the rainfall time series, we stored the predictive model made using HoltWinters() in the variable “rainseriesforecasts”. You specify how many further time points you want to make forecasts for by using the “h” parameter in forecast.HoltWinters(). For example, to make a forecast of rainfall for the years 1814-1820 (8 more years) using forecast.HoltWinters(), we type:

> rainseriesforecasts2 <- forecast.HoltWinters(rainseriesforecasts, h=8) > rainseriesforecasts2 Point Forecast Lo 80 Hi 80 Lo 95 Hi 95 1913 24.67819 19.17493 30.18145 16.26169 33.09470 1914 24.67819 19.17333 30.18305 16.25924 33.09715 1915 24.67819 19.17173 30.18465 16.25679 33.09960 1916 24.67819 19.17013 30.18625 16.25434 33.10204 1917 24.67819 19.16853 30.18785 16.25190 33.10449 1918 24.67819 19.16694 30.18945 16.24945 33.10694 1919 24.67819 19.16534 30.19105 16.24701 33.10938 1920 24.67819 19.16374 30.19265 16.24456 33.11182

The forecast.HoltWinters() function gives you the forecast for a year, a 80% prediction interval for the forecast, and a 95% prediction interval for the forecast. For example, the forecasted rainfall for 1920 is about 24.68 inches, with a 95% prediction interval of (16.24, 33.11).

To plot the predictions made by forecast.HoltWinters(), we can use the “plot.forecast()” function:

> plot.forecast(rainseriesforecasts2)

Here the forecasts for 1913-1920 are plotted as a blue line, the 80% prediction interval as an orange shaded area, and the 95% prediction interval as a yellow shaded area.

The ‘forecast errors’ are calculated as the observed values minus predicted values, for each time point. We can only calculate the forecast errors for the time period covered by our original time series, which is 1813-1912 for the rainfall data. As mentioned above, one measure of the accuracy of the predictive model is the sum-of-squared-errors (SSE) for the in-sample forecast errors.

The in-sample forecast errors are stored in the named element “residuals” of the list variable returned by forecast.HoltWinters(). If the predictive model cannot be improved upon, there should be no correlations between forecast errors for successive predictions. In other words, if there are correlations between forecast errors for successive predictions, it is likely that the simple exponential smoothing forecasts could be improved upon by another forecasting technique.

To figure out whether this is the case, we can obtain a correlogram of the in-sample forecast errors for lags 1-20. We can calculate a correlogram of the forecast errors using the “acf()” function in R. To specify the maximum lag that we want to look at, we use the “lag.max” parameter in acf().

For example, to calculate a correlogram of the in-sample forecast errors for the London rainfall data for lags 1-20, we type:

> acf(rainseriesforecasts2$residuals, lag.max=20)

You can see from the sample correlogram that the autocorrelation at lag 3 is just touching the significance bounds. To test whether there is significant evidence for non-zero correlations at lags 1-20, we can carry out a Ljung-Box test. This can be done in R using the “Box.test()”, function. The maximum lag that we want to look at is specified using the “lag” parameter in the Box.test() function. For example, to test whether there are non-zero autocorrelations at lags 1-20, for the in-sample forecast errors for London rainfall data, we type:

> Box.test(rainseriesforecasts2$residuals, lag=20, type="Ljung-Box") Box-Ljung test data: rainseriesforecasts2$residuals X-squared = 17.4008, df = 20, p-value = 0.6268

Here the Ljung-Box test statistic is 17.4, and the p-value is 0.6, so there is little evidence of non-zero autocorrelations in the in-sample forecast errors at lags 1-20.

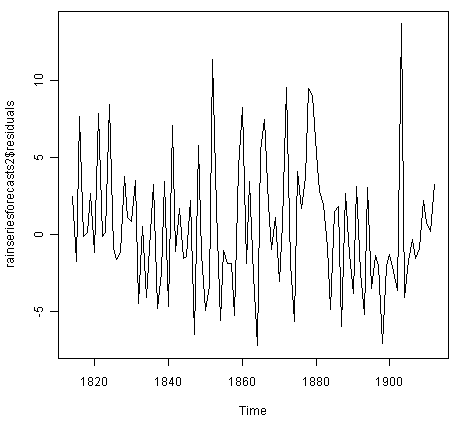

To be sure that the predictive model cannot be improved upon, it is also a good idea to check whether the forecast errors are normally distributed with mean zero and constant variance. To check whether the forecast errors have constant variance, we can make a time plot of the in-sample forecast errors:

> plot.ts(rainseriesforecasts2$residuals)

The plot shows that the in-sample forecast errors seem to have roughly constant variance over time, although the size of the fluctuations in the start of the time series (1820-1830) may be slightly less than that at later dates (eg. 1840-1850).

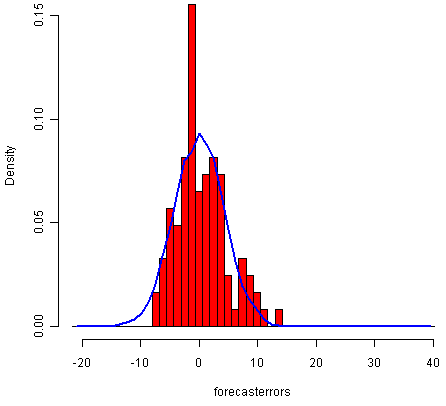

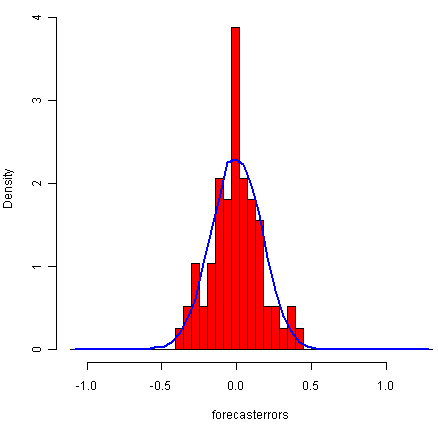

To check whether the forecast errors are normally distributed with mean zero, we can plot a histogram of the forecast errors, with an overlaid normal curve that has mean zero and the same standard deviation as the distribution of forecast errors. To do this, we can define an R function “plotForecastErrors()”, below:

> plotForecastErrors <- function(forecasterrors) { # make a histogram of the forecast errors: mybinsize <- IQR(forecasterrors)/4 mysd <- sd(forecasterrors) mymin <- min(forecasterrors) - mysd*5 mymax <- max(forecasterrors) + mysd*3 # generate normally distributed data with mean 0 and standard deviation mysd mynorm <- rnorm(10000, mean=0, sd=mysd) mymin2 <- min(mynorm) mymax2 <- max(mynorm) if (mymin2 < mymin) { mymin <- mymin2 } if (mymax2 > mymax) { mymax <- mymax2 } # make a red histogram of the forecast errors, with the normally distributed data overlaid: mybins <- seq(mymin, mymax, mybinsize) hist(forecasterrors, col="red", freq=FALSE, breaks=mybins) # freq=FALSE ensures the area under the histogram = 1 # generate normally distributed data with mean 0 and standard deviation mysd myhist <- hist(mynorm, plot=FALSE, breaks=mybins) # plot the normal curve as a blue line on top of the histogram of forecast errors: points(myhist$mids, myhist$density, type="l", col="blue", lwd=2) }

You will have to copy the function above into R in order to use it. You can then use plotForecastErrors() to plot a histogram (with overlaid normal curve) of the forecast errors for the rainfall predictions:

> plotForecastErrors(rainseriesforecasts2$residuals)

The plot shows that the distribution of forecast errors is roughly centred on zero, and is more or less normally distributed, although it seems to be slightly skewed to the right compared to a normal curve. However, the right skew is relatively small, and so it is plausible that the forecast errors are normally distributed with mean zero.

The Ljung-Box test showed that there is little evidence of non-zero autocorrelations in the in-sample forecast errors, and the distribution of forecast errors seems to be normally distributed with mean zero. This suggests that the simple exponential smoothing method provides an adequate predictive model for London rainfall, which probably cannot be improved upon. Furthermore, the assumptions that the 80% and 95% predictions intervals were based upon (that there are no autocorrelations in the forecast errors, and the forecast errors are normally distributed with mean zero and constant variance) are probably valid.

Holt’s Exponential Smoothing

If you have a time series that can be described using an additive model with increasing or decreasing trend and no seasonality, you can use Holt’s exponential smoothing to make short-term forecasts.

Holt’s exponential smoothing estimates the level and slope at the current time point. Smoothing is controlled by two parameters, alpha, for the estimate of the level at the current time point, and beta for the estimate of the slope b of the trend component at the current time point. As with simple exponential smoothing, the paramters alpha and beta have values between 0 and 1, and values that are close to 0 mean that little weight is placed on the most recent observations when making forecasts of future values.

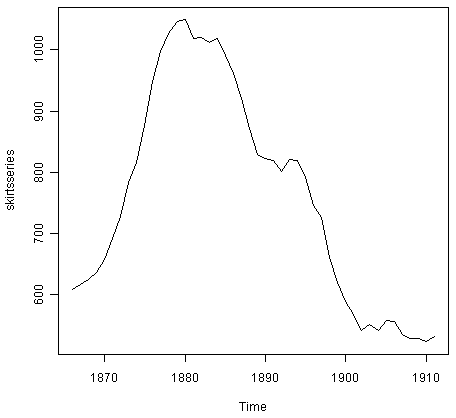

An example of a time series that can probably be described using an additive model with a trend and no seasonality is the time series of the annual diameter of women’s skirts at the hem, from 1866 to 1911. The data is available in the file http://robjhyndman.com/tsdldata/roberts/skirts.dat (original data from Hipel and McLeod, 1994).

We can read in and plot the data in R by typing:

> skirts <- scan("http://robjhyndman.com/tsdldata/roberts/skirts.dat",skip=5) Read 46 items > skirtsseries <- ts(skirts,start=c(1866)) > plot.ts(skirtsseries)

We can see from the plot that there was an increase in hem diameter from about 600 in 1866 to about 1050 in 1880, and that afterwards the hem diameter decreased to about 520 in 1911.

To make forecasts, we can fit a predictive model using the HoltWinters() function in R. To use HoltWinters() for Holt’s exponential smoothing, we need to set the parameter gamma=FALSE (the gamma parameter is used for Holt-Winters exponential smoothing, as described below).

For example, to use Holt’s exponential smoothing to fit a predictive model for skirt hem diameter, we type:

> skirtsseriesforecasts <- HoltWinters(skirtsseries, gamma=FALSE) > skirtsseriesforecasts Smoothing parameters: alpha: 0.8383481 beta : 1 gamma: FALSE Coefficients: [,1] a 529.308585 b 5.690464 > skirtsseriesforecasts$SSE [1] 16954.18

The estimated value of alpha is 0.84, and of beta is 1.00. These are both high, telling us that both the estimate of the current value of the level, and of the slope b of the trend component, are based mostly upon very recent observations in the time series. This makes good intuitive sense, since the level and the slope of the time series both change quite a lot over time. The value of the sum-of-squared-errors for the in-sample forecast errors is 16954.

We can plot the original time series as a black line, with the forecasted values as a red line on top of that, by typing:

> plot(skirtsseriesforecasts)

We can see from the picture that the in-sample forecasts agree pretty well with the observed values, although they tend to lag behind the observed values a little bit.

If you wish, you can specify the initial values of the level and the slope b of the trend component by using the “l.start” and “b.start” arguments for the HoltWinters() function. It is common to set the initial value of the level to the first value in the time series (608 for the skirts data), and the initial value of the slope to the second value minus the first value (9 for the skirts data). For example, to fit a predictive model to the skirt hem data using Holt’s exponential smoothing, with initial values of 608 for the level and 9 for the slope b of the trend component, we type:

> HoltWinters(skirtsseries, gamma=FALSE, l.start=608, b.start=9)

As for simple exponential smoothing, we can make forecasts for future times not covered by the original time series by using the forecast.HoltWinters() function in the “forecast” package. For example, our time series data for skirt hems was for 1866 to 1911, so we can make predictions for 1912 to 1930 (19 more data points), and plot them, by typing:

> skirtsseriesforecasts2 <- forecast.HoltWinters(skirtsseriesforecasts, h=19) > plot.forecast(skirtsseriesforecasts2)

The forecasts are shown as a blue line, with the 80% prediction intervals as an orange shaded area, and the 95% prediction intervals as a yellow shaded area.

As for simple exponential smoothing, we can check whether the predictive model could be improved upon by checking whether the in-sample forecast errors show non-zero autocorrelations at lags 1-20. For example, for the skirt hem data, we can make a correlogram, and carry out the Ljung-Box test, by typing:

> acf(skirtsseriesforecasts2$residuals, lag.max=20) > Box.test(skirtsseriesforecasts2$residuals, lag=20, type="Ljung-Box") Box-Ljung test data: skirtsseriesforecasts2$residuals X-squared = 19.7312, df = 20, p-value = 0.4749

Here the correlogram shows that the sample autocorrelation for the in-sample forecast errors at lag 5 exceeds the significance bounds. However, we would expect one in 20 of the autocorrelations for the first twenty lags to exceed the 95% significance bounds by chance alone. Indeed, when we carry out the Ljung-Box test, the p-value is 0.47, indicating that there is little evidence of non-zero autocorrelations in the in-sample forecast errors at lags 1-20.

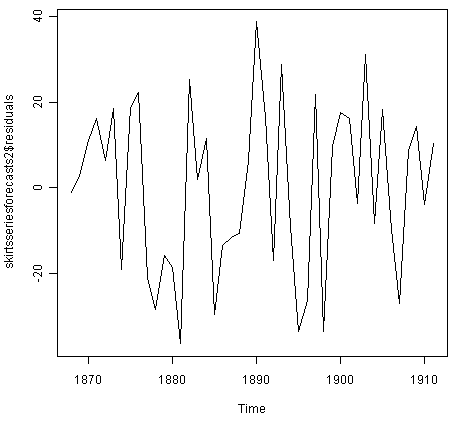

As for simple exponential smoothing, we should also check that the forecast errors have constant variance over time, and are normally distributed with mean zero. We can do this by making a time plot of forecast errors, and a histogram of the distribution of forecast errors with an overlaid normal curve:

> plot.ts(skirtsseriesforecasts2$residuals) # make a time plot > plotForecastErrors(skirtsseriesforecasts2$residuals) # make a histogram

The time plot of forecast errors shows that the forecast errors have roughly constant variance over time. The histogram of forecast errors show that it is plausible that the forecast errors are normally distributed with mean zero and constant variance.

Thus, the Ljung-Box test shows that there is little evidence of autocorrelations in the forecast errors, while the time plot and histogram of forecast errors show that it is plausible that the forecast errors are normally distributed with mean zero and constant variance. Therefore, we can conclude that Holt’s exponential smoothing provides an adequate predictive model for skirt hem diameters, which probably cannot be improved upon. In addition, it means that the assumptions that the 80% and 95% predictions intervals were based upon are probably valid.

Holt-Winters Exponential Smoothing

If you have a time series that can be described using an additive model with increasing or decreasing trend and seasonality, you can use Holt-Winters exponential smoothing to make short-term forecasts.

Holt-Winters exponential smoothing estimates the level, slope and seasonal component at the current time point. Smoothing is controlled by three parameters: alpha, beta, and gamma, for the estimates of the level, slope b of the trend component, and the seasonal component, respectively, at the current time point. The parameters alpha, beta and gamma all have values between 0 and 1, and values that are close to 0 mean that relatively little weight is placed on the most recent observations when making forecasts of future values.

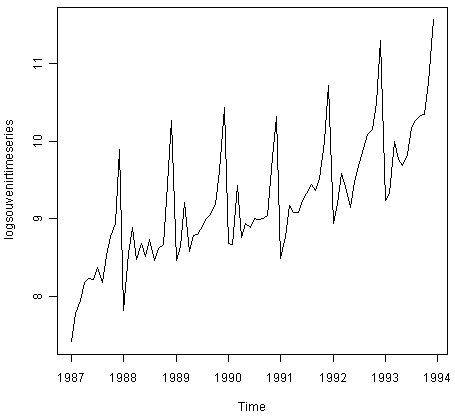

An example of a time series that can probably be described using an additive model with a trend and seasonality is the time series of the log of monthly sales for the souvenir shop at a beach resort town in Queensland, Australia (discussed above):

To make forecasts, we can fit a predictive model using the HoltWinters() function. For example, to fit a predictive model for the log of the monthly sales in the souvenir shop, we type:

> logsouvenirtimeseries <- log(souvenirtimeseries) > souvenirtimeseriesforecasts <- HoltWinters(logsouvenirtimeseries) > souvenirtimeseriesforecasts Holt-Winters exponential smoothing with trend and additive seasonal component. Smoothing parameters: alpha: 0.413418 beta : 0 gamma: 0.9561275 Coefficients: [,1] a 10.37661961 b 0.02996319 s1 -0.80952063 s2 -0.60576477 s3 0.01103238 s4 -0.24160551 s5 -0.35933517 s6 -0.18076683 s7 0.07788605 s8 0.10147055 s9 0.09649353 s10 0.05197826 s11 0.41793637 s12 1.18088423 > souvenirtimeseriesforecasts$SSE 2.011491

The estimated values of alpha, beta and gamma are 0.41, 0.00, and 0.96, respectively. The value of alpha (0.41) is relatively low, indicating that the estimate of the level at the current time point is based upon both recent observations and some observations in the more distant past. The value of beta is 0.00, indicating that the estimate of the slope b of the trend component is not updated over the time series, and instead is set equal to its initial value. This makes good intuitive sense, as the level changes quite a bit over the time series, but the slope b of the trend component remains roughly the same. In contrast, the value of gamma (0.96) is high, indicating that the estimate of the seasonal component at the current time point is just based upon very recent observations.

As for simple exponential smoothing and Holt’s exponential smoothing, we can plot the original time series as a black line, with the forecasted values as a red line on top of that:

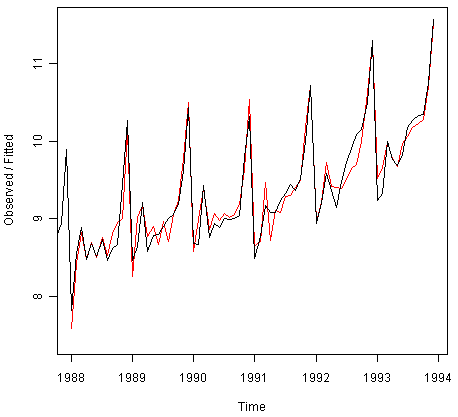

> plot(souvenirtimeseriesforecasts)

We see from the plot that the Holt-Winters exponential method is very successful in predicting the seasonal peaks, which occur roughly in November every year.

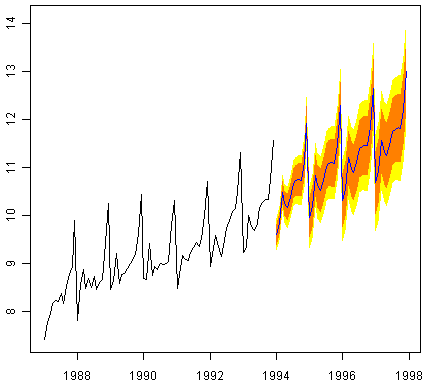

To make forecasts for future times not included in the original time series, we use the “forecast.HoltWinters()” function in the “forecast” package. For example, the original data for the souvenir sales is from January 1987 to December 1993. If we wanted to make forecasts for January 1994 to December 1998 (48 more months), and plot the forecasts, we would type:

> souvenirtimeseriesforecasts2 <- forecast.HoltWinters(souvenirtimeseriesforecasts, h=48) > plot.forecast(souvenirtimeseriesforecasts2)

The forecasts are shown as a blue line, and the orange and yellow shaded areas show 80% and 95% prediction intervals, respectively.

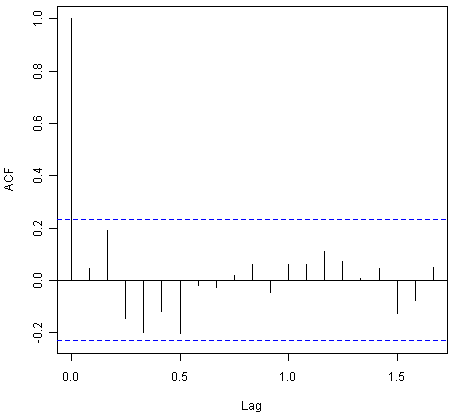

We can investigate whether the predictive model can be improved upon by checking whether the in-sample forecast errors show non-zero autocorrelations at lags 1-20, by making a correlogram and carrying out the Ljung-Box test:

> acf(souvenirtimeseriesforecasts2$residuals, lag.max=20) > Box.test(souvenirtimeseriesforecasts2$residuals, lag=20, type="Ljung-Box") Box-Ljung test data: souvenirtimeseriesforecasts2$residuals X-squared = 17.5304, df = 20, p-value = 0.6183

The correlogram shows that the autocorrelations for the in-sample forecast errors do not exceed the significance bounds for lags 1-20. Furthermore, the p-value for Ljung-Box test is 0.6, indicating that there is little evidence of non-zero autocorrelations at lags 1-20.

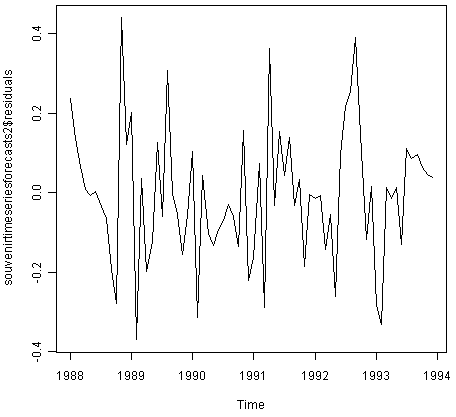

We can check whether the forecast errors have constant variance over time, and are normally distributed with mean zero, by making a time plot of the forecast errors and a histogram (with overlaid normal curve):

> plot.ts(souvenirtimeseriesforecasts2$residuals) # make a time plot > plotForecastErrors(souvenirtimeseriesforecasts2$residuals) # make a histogram

From the time plot, it appears plausible that the forecast errors have constant variance over time. From the histogram of forecast errors, it seems plausible that the forecast errors are normally distributed with mean zero.

Thus,there is little evidence of autocorrelation at lags 1-20 for the forecast errors, and the forecast errors appear to be normally distributed with mean zero and constant variance over time. This suggests that Holt-Winters exponential smoothing provides an adequate predictive model of the log of sales at the souvenir shop, which probably cannot be improved upon. Furthermore, the assumptions upon which the prediction intervals were based are probably valid.

ARIMA Models

Exponential smoothing methods are useful for making forecasts, and make no assumptions about the correlations between successive values of the time series. However, if you want to make prediction intervals for forecasts made using exponential smoothing methods, the prediction intervals require that the forecast errors are uncorrelated and are normally distributed with mean zero and constant variance.

While exponential smoothing methods do not make any assumptions about correlations between successive values of the time series, in some cases you can make a better predictive model by taking correlations in the data into account. Autoregressive Integrated Moving Average (ARIMA) models include an explicit statistical model for the irregular component of a time series, that allows for non-zero autocorrelations in the irregular component.

Differencing a Time Series

ARIMA models are defined for stationary time series. Therefore, if you start off with a non-stationary time series, you will first need to ‘difference’ the time series until you obtain a stationary time series. If you have to difference the time series d times to obtain a stationary series, then you have an ARIMA(p,d,q) model, where d is the order of differencing used.

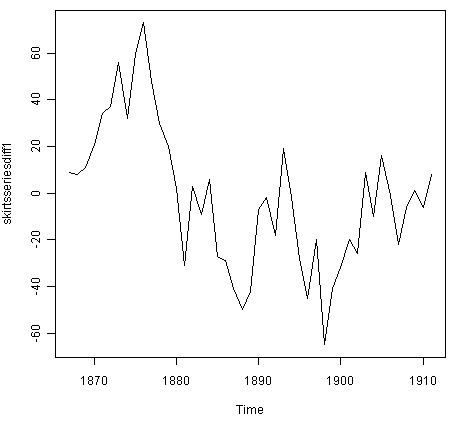

You can difference a time series using the “diff()” function in R. For example, the time series of the annual diameter of women’s skirts at the hem, from 1866 to 1911 is not stationary in mean, as the level changes a lot over time:

We can difference the time series (which we stored in “skirtsseries”, see above) once, and plot the differenced series, by typing:

> skirtsseriesdiff1 <- diff(skirtsseries, differences=1) > plot.ts(skirtsseriesdiff1)

The resulting time series of first differences (above) does not appear to be stationary in mean. Therefore, we can difference the time series twice, to see if that gives us a stationary time series:

> skirtsseriesdiff2 <- diff(skirtsseries, differences=2) > plot.ts(skirtsseriesdiff2)

Formal tests for stationarity

Formal tests for stationarity called “unit root tests” are available in the fUnitRoots package, available on CRAN, but will not be discussed here.

The time series of second differences (above) does appear to be stationary in mean and variance, as the level of the series stays roughly constant over time, and the variance of the series appears roughly constant over time. Thus, it appears that we need to difference the time series of the diameter of skirts twice in order to achieve a stationary series.

If you need to difference your original time series data d times in order to obtain a stationary time series, this means that you can use an ARIMA(p,d,q) model for your time series, where d is the order of differencing used. For example, for the time series of the diameter of women’s skirts, we had to difference the time series twice, and so the order of differencing (d) is 2. This means that you can use an ARIMA(p,2,q) model for your time series. The next step is to figure out the values of p and q for the ARIMA model.

Another example is the time series of the age of death of the successive kings of England (see above):

From the time plot (above), we can see that the time series is not stationary in mean. To calculate the time series of first differences, and plot it, we type:

> kingtimeseriesdiff1 <- diff(kingstimeseries, differences=1) > plot.ts(kingtimeseriesdiff1)

The time series of first differences appears to be stationary in mean and variance, and so an ARIMA(p,1,q) model is probably appropriate for the time series of the age of death of the kings of England. By taking the time series of first differences, we have removed the trend component of the time series of the ages at death of the kings, and are left with an irregular component. We can now examine whether there are correlations between successive terms of this irregular component; if so, this could help us to make a predictive model for the ages at death of the kings.

Selecting a Candidate ARIMA Model

If your time series is stationary, or if you have transformed it to a stationary time series by differencing d times, the next step is to select the appropriate ARIMA model, which means finding the values of most appropriate values of p and q for an ARIMA(p,d,q) model. To do this, you usually need to examine the correlogram and partial correlogram of the stationary time series.

To plot a correlogram and partial correlogram, we can use the “acf()” and “pacf()” functions in R, respectively. To get the actual values of the autocorrelations and partial autocorrelations, we set “plot=FALSE” in the “acf()” and “pacf()” functions.

Example of the Ages at Death of the Kings of England

For example, to plot the correlogram for lags 1-20 of the once differenced time series of the ages at death of the kings of England, and to get the values of the autocorrelations, we type:

> acf(kingtimeseriesdiff1, lag.max=20) # plot a correlogram > acf(kingtimeseriesdiff1, lag.max=20, plot=FALSE) # get the autocorrelation values Autocorrelations of series 'kingtimeseriesdiff1', by lag 0 1 2 3 4 5 6 7 8 9 10 1.000 -0.360 -0.162 -0.050 0.227 -0.042 -0.181 0.095 0.064 -0.116 -0.071 11 12 13 14 15 16 17 18 19 20 0.206 -0.017 -0.212 0.130 0.114 -0.009 -0.192 0.072 0.113 -0.093

We see from the correlogram that the autocorrelation at lag 1 (-0.360) exceeds the significance bounds, but all other autocorrelations between lags 1-20 do not exceed the significance bounds.

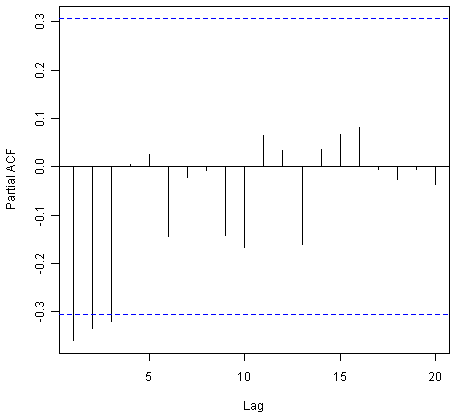

To plot the partial correlogram for lags 1-20 for the once differenced time series of the ages at death of the English kings, and get the values of the partial autocorrelations, we use the “pacf()” function, by typing:

> pacf(kingtimeseriesdiff1, lag.max=20) # plot a partial correlogram > pacf(kingtimeseriesdiff1, lag.max=20, plot=FALSE) # get the partial autocorrelation values Partial autocorrelations of series 'kingtimeseriesdiff1', by lag 1 2 3 4 5 6 7 8 9 10 11 -0.360 -0.335 -0.321 0.005 0.025 -0.144 -0.022 -0.007 -0.143 -0.167 0.065 12 13 14 15 16 17 18 19 20 0.034 -0.161 0.036 0.066 0.081 -0.005 -0.027 -0.006 -0.037

The partial correlogram shows that the partial autocorrelations at lags 1, 2 and 3 exceed the significance bounds, are negative, and are slowly decreasing in magnitude with increasing lag (lag 1: -0.360, lag 2: -0.335, lag 3:-0.321). The partial autocorrelations tail off to zero after lag 3.

Since the correlogram is zero after lag 1, and the partial correlogram tails off to zero after lag 3, this means that the following ARMA (autoregressive moving average) models are possible for the time series of first differences:

- an ARMA(3,0) model, that is, an autoregressive model of order p=3, since the partial autocorrelogram is zero after lag 3, and the autocorrelogram tails off to zero (although perhaps too abruptly for this model to be appropriate)

- an ARMA(0,1) model, that is, a moving average model of order q=1, since the autocorrelogram is zero after lag 1 and the partial autocorrelogram tails off to zero

- an ARMA(p,q) model, that is, a mixed model with p and q greater than 0, since the autocorrelogram and partial correlogram tail off to zero (although the correlogram probably tails off to zero too abruptly for this model to be appropriate)

We use the principle of parsimony to decide which model is best: that is, we assume that the model with the fewest parameters is best. The ARMA(3,0) model has 3 parameters, the ARMA(0,1) model has 1 parameter, and the ARMA(p,q) model has at least 2 parameters. Therefore, the ARMA(0,1) model is taken as the best model.

An ARMA(0,1) model is a moving average model of order 1, or MA(1) model. This model can be written as: X_t - mu = Z_t - (theta * Z_t-1), where X_t is the stationary time series we are studying (the first differenced series of ages at death of English kings), mu is the mean of time series X_t, Z_t is white noise with mean zero and constant variance, and theta is a parameter that can be estimated.

A MA (moving average) model is usually used to model a time series that shows short-term dependencies between successive observations. Intuitively, it makes good sense that a MA model can be used to describe the irregular component in the time series of ages at death of English kings, as we might expect the age at death of a particular English king to have some effect on the ages at death of the next king or two, but not much effect on the ages at death of kings that reign much longer after that.

Shortcut: the auto.arima() function

The auto.arima() function can be used to find the appropriate ARIMA model, eg., type “library(forecast)”, then “auto.arima(kings)”. The output says an appropriate model is ARIMA(0,1,1).

Since an ARMA(0,1) model (with p=0, q=1) is taken to be the best candidate model for the time series of first differences of the ages at death of English kings, then the original time series of the ages of death can be modelled using an ARIMA(0,1,1) model (with p=0, d=1, q=1, where d is the order of differencing required).

Example of the Volcanic Dust Veil in the Northern Hemisphere

Let’s take another example of selecting an appropriate ARIMA model. The file file http://robjhyndman.com/tsdldata/annual/dvi.dat contains data on the volcanic dust veil index in the northern hemisphere, from 1500-1969 (original data from Hipel and Mcleod, 1994). This is a measure of the impact of volcanic eruptions’ release of dust and aerosols into the environment. We can read it into R and make a time plot by typing:

> volcanodust <- scan("http://robjhyndman.com/tsdldata/annual/dvi.dat", skip=1) Read 470 items > volcanodustseries <- ts(volcanodust,start=c(1500)) > plot.ts(volcanodustseries)

From the time plot, it appears that the random fluctuations in the time series are roughly constant in size over time, so an additive model is probably appropriate for describing this time series.

Furthermore, the time series appears to be stationary in mean and variance, as its level and variance appear to be roughly constant over time. Therefore, we do not need to difference this series in order to fit an ARIMA model, but can fit an ARIMA model to the original series (the order of differencing required, d, is zero here).

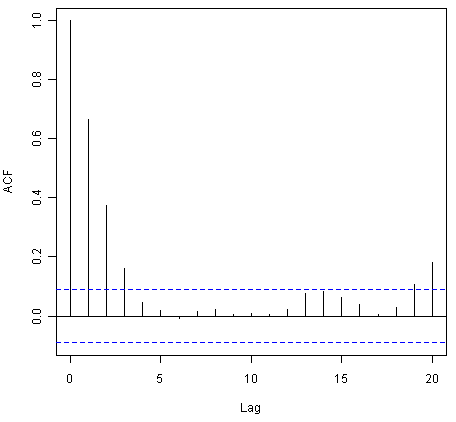

We can now plot a correlogram and partial correlogram for lags 1-20 to investigate what ARIMA model to use:

> acf(volcanodustseries, lag.max=20) # plot a correlogram > acf(volcanodustseries, lag.max=20, plot=FALSE) # get the values of the autocorrelations Autocorrelations of series 'volcanodustseries', by lag 0 1 2 3 4 5 6 7 8 9 10 1.000 0.666 0.374 0.162 0.046 0.017 -0.007 0.016 0.021 0.006 0.010 11 12 13 14 15 16 17 18 19 20 0.004 0.024 0.075 0.082 0.064 0.039 0.005 0.028 0.108 0.182

We see from the correlogram that the autocorrelations for lags 1, 2 and 3 exceed the significance bounds, and that the autocorrelations tail off to zero after lag 3. The autocorrelations for lags 1, 2, 3 are positive, and decrease in magnitude with increasing lag (lag 1: 0.666, lag 2: 0.374, lag 3: 0.162).

The autocorrelation for lags 19 and 20 exceed the significance bounds too, but it is likely that this is due to chance, since they just exceed the significance bounds (especially for lag 19), the autocorrelations for lags 4-18 do not exceed the signifiance bounds, and we would expect 1 in 20 lags to exceed the 95% significance bounds by chance alone.

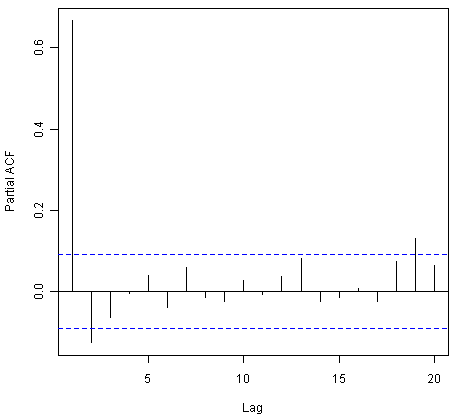

> pacf(volcanodustseries, lag.max=20) > pacf(volcanodustseries, lag.max=20, plot=FALSE) Partial autocorrelations of series 'volcanodustseries', by lag 1 2 3 4 5 6 7 8 9 10 11 0.666 -0.126 -0.064 -0.005 0.040 -0.039 0.058 -0.016 -0.025 0.028 -0.008 12 13 14 15 16 17 18 19 20 0.036 0.082 -0.025 -0.014 0.008 -0.025 0.073 0.131 0.063

From the partial autocorrelogram, we see that the partial autocorrelation at lag 1 is positive and exceeds the significance bounds (0.666), while the partial autocorrelation at lag 2 is negative and also exceeds the significance bounds (-0.126). The partial autocorrelations tail off to zero after lag 2.

Since the correlogram tails off to zero after lag 3, and the partial correlogram is zero after lag 2, the following ARMA models are possible for the time series:

- an ARMA(2,0) model, since the partial autocorrelogram is zero after lag 2, and the correlogram tails off to zero after lag 3, and the partial correlogram is zero after lag 2

- an ARMA(0,3) model, since the autocorrelogram is zero after lag 3, and the partial correlogram tails off to zero (although perhaps too abruptly for this model to be appropriate)

- an ARMA(p,q) mixed model, since the correlogram and partial correlogram tail off to zero (although the partial correlogram perhaps tails off too abruptly for this model to be appropriate)

Shortcut: the auto.arima() function

Again, we can use auto.arima() to find an appropriate model, by typing “auto.arima(volcanodust)”, which gives us ARIMA(1,0,2), which has 3 parameters. However, different criteria can be used to select a model (see auto.arima() help page). If we use the “bic” criterion, which penalises the number of parameters, we get ARIMA(2,0,0), which is ARMA(2,0): “auto.arima(volcanodust,ic=”bic”)”.

The ARMA(2,0) model has 2 parameters, the ARMA(0,3) model has 3 parameters, and the ARMA(p,q) model has at least 2 parameters. Therefore, using the principle of parsimony, the ARMA(2,0) model and ARMA(p,q) model are equally good candidate models.

An ARMA(2,0) model is an autoregressive model of order 2, or AR(2) model. This model can be written as: X_t - mu = (Beta1 * (X_t-1 - mu)) + (Beta2 * (Xt-2 - mu)) + Z_t, where X_t is the stationary time series we are studying (the time series of volcanic dust veil index), mu is the mean of time series X_t, Beta1 and Beta2 are parameters to be estimated, and Z_t is white noise with mean zero and constant variance.

An AR (autoregressive) model is usually used to model a time series which shows longer term dependencies between successive observations. Intuitively, it makes sense that an AR model could be used to describe the time series of volcanic dust veil index, as we would expect volcanic dust and aerosol levels in one year to affect those in much later years, since the dust and aerosols are unlikely to disappear quickly.

If an ARMA(2,0) model (with p=2, q=0) is used to model the time series of volcanic dust veil index, it would mean that an ARIMA(2,0,0) model can be used (with p=2, d=0, q=0, where d is the order of differencing required). Similarly, if an ARMA(p,q) mixed model is used, where p and q are both greater than zero, than an ARIMA(p,0,q) model can be used.

Forecasting Using an ARIMA Model

Once you have selected the best candidate ARIMA(p,d,q) model for your time series data, you can estimate the parameters of that ARIMA model, and use that as a predictive model for making forecasts for future values of your time series.

You can estimate the parameters of an ARIMA(p,d,q) model using the “arima()” function in R.

Example of the Ages at Death of the Kings of England

For example, we discussed above that an ARIMA(0,1,1) model seems a plausible model for the ages at deaths of the kings of England. You can specify the values of p, d and q in the ARIMA model by using the “order” argument of the “arima()” function in R. To fit an ARIMA(p,d,q) model to this time series (which we stored in the variable “kingstimeseries”, see above), we type:

> kingstimeseriesarima <- arima(kingstimeseries, order=c(0,1,1)) # fit an ARIMA(0,1,1) model > kingstimeseriesarima ARIMA(0,1,1) Coefficients: ma1 -0.7218 s.e. 0.1208 sigma^2 estimated as 230.4: log likelihood = -170.06 AIC = 344.13 AICc = 344.44 BIC = 347.56

As mentioned above, if we are fitting an ARIMA(0,1,1) model to our time series, it means we are fitting an an ARMA(0,1) model to the time series of first differences. An ARMA(0,1) model can be written X_t - mu = Z_t - (theta * Z_t-1), where theta is a parameter to be estimated. From the output of the “arima()” R function (above), the estimated value of theta (given as ‘ma1’ in the R output) is -0.7218 in the case of the ARIMA(0,1,1) model fitted to the time series of ages at death of kings.

Specifying the confidence level for prediction intervals

You can specify the confidence level for prediction intervals in forecast.Arima() by using the “level” argument. For example, to get a 99.5% prediction interval, we would type “forecast.Arima(kingstimeseriesarima, h=5, level=c(99.5))”.

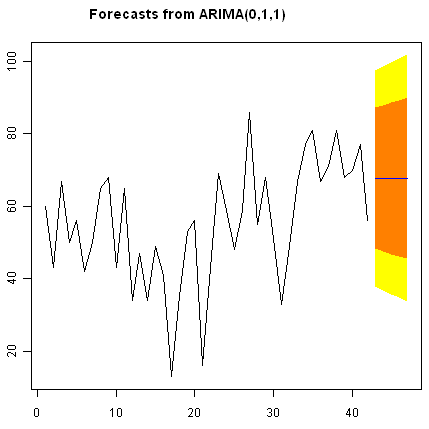

We can then use the ARIMA model to make forecasts for future values of the time series, using the “forecast.Arima()” function in the “forecast” R package. For example, to forecast the ages at death of the next five English kings, we type:

> library("forecast") # load the "forecast" R library > kingstimeseriesforecasts <- forecast.Arima(kingstimeseriesarima, h=5) > kingstimeseriesforecasts Point Forecast Lo 80 Hi 80 Lo 95 Hi 95 43 67.75063 48.29647 87.20479 37.99806 97.50319 44 67.75063 47.55748 87.94377 36.86788 98.63338 45 67.75063 46.84460 88.65665 35.77762 99.72363 46 67.75063 46.15524 89.34601 34.72333 100.77792 47 67.75063 45.48722 90.01404 33.70168 101.79958

The original time series for the English kings includes the ages at death of 42 English kings. The forecast.Arima() function gives us a forecast of the age of death of the next five English kings (kings 43-47), as well as 80% and 95% prediction intervals for those predictions. The age of death of the 42nd English king was 56 years (the last observed value in our time series), and the ARIMA model gives the forecasted age at death of the next five kings as 67.8 years.

We can plot the observed ages of death for the first 42 kings, as well as the ages that would be predicted for these 42 kings and for the next 5 kings using our ARIMA(0,1,1) model, by typing:

> plot.forecast(kingstimeseriesforecasts)

As in the case of exponential smoothing models, it is a good idea to investigate whether the forecast errors of an ARIMA model are normally distributed with mean zero and constant variance, and whether the are correlations between successive forecast errors.

For example, we can make a correlogram of the forecast errors for our ARIMA(0,1,1) model for the ages at death of kings, and perform the Ljung-Box test for lags 1-20, by typing:

> acf(kingstimeseriesforecasts$residuals, lag.max=20) > Box.test(kingstimeseriesforecasts$residuals, lag=20, type="Ljung-Box") Box-Ljung test data: kingstimeseriesforecasts$residuals X-squared = 13.5844, df = 20, p-value = 0.851

Since the correlogram shows that none of the sample autocorrelations for lags 1-20 exceed the significance bounds, and the p-value for the Ljung-Box test is 0.9, we can conclude that there is very little evidence for non-zero autocorrelations in the forecast errors at lags 1-20.

To investigate whether the forecast errors are normally distributed with mean zero and constant variance, we can make a time plot and histogram (with overlaid normal curve) of the forecast errors:

> plot.ts(kingstimeseriesforecasts$residuals) # make time plot of forecast errors > plotForecastErrors(kingstimeseriesforecasts$residuals) # make a histogram

The time plot of the in-sample forecast errors shows that the variance of the forecast errors seems to be roughly constant over time (though perhaps there is slightly higher variance for the second half of the time series). The histogram of the time series shows that the forecast errors are roughly normally distributed and the mean seems to be close to zero. Therefore, it is plausible that the forecast errors are normally distributed with mean zero and constant variance.

Since successive forecast errors do not seem to be correlated, and the forecast errors seem to be normally distributed with mean zero and constant variance, the ARIMA(0,1,1) does seem to provide an adequate predictive model for the ages at death of English kings.

Example of the Volcanic Dust Veil in the Northern Hemisphere

We discussed above that an appropriate ARIMA model for the time series of volcanic dust veil index may be an ARIMA(2,0,0) model. To fit an ARIMA(2,0,0) model to this time series, we can type:

> volcanodustseriesarima <- arima(volcanodustseries, order=c(2,0,0)) > volcanodustseriesarima ARIMA(2,0,0) with non-zero mean Coefficients: ar1 ar2 intercept 0.7533 -0.1268 57.5274 s.e. 0.0457 0.0458 8.5958 sigma^2 estimated as 4870: log likelihood = -2662.54 AIC = 5333.09 AICc = 5333.17 BIC = 5349.7

As mentioned above, an ARIMA(2,0,0) model can be written as: written as: X_t - mu = (Beta1 * (X_t-1 - mu)) + (Beta2 * (Xt-2 - mu)) + Z_t, where Beta1 and Beta2 are parameters to be estimated. The output of the arima() function tells us that Beta1 and Beta2 are estimated as 0.7533 and -0.1268 here (given as ar1 and ar2 in the output of arima()).

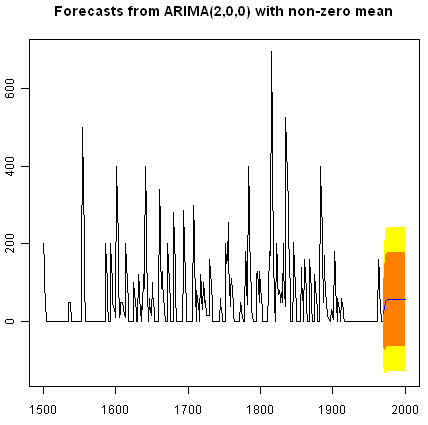

Now we have fitted the ARIMA(2,0,0) model, we can use the “forecast.ARIMA()” model to predict future values of the volcanic dust veil index. The original data includes the years 1500-1969. To make predictions for the years 1970-2000 (31 more years), we type:

> volcanodustseriesforecasts <- forecast.Arima(volcanodustseriesarima, h=31) > volcanodustseriesforecasts Point Forecast Lo 80 Hi 80 Lo 95 Hi 95 1970 21.48131 -67.94860 110.9112 -115.2899 158.2526 1971 37.66419 -74.30305 149.6314 -133.5749 208.9033 1972 47.13261 -71.57070 165.8359 -134.4084 228.6737 1973 52.21432 -68.35951 172.7881 -132.1874 236.6161 1974 54.84241 -66.22681 175.9116 -130.3170 240.0018 1975 56.17814 -65.01872 177.3750 -129.1765 241.5327 1976 56.85128 -64.37798 178.0805 -128.5529 242.2554 1977 57.18907 -64.04834 178.4265 -128.2276 242.6057 1978 57.35822 -63.88124 178.5977 -128.0615 242.7780 1979 57.44283 -63.79714 178.6828 -127.9777 242.8634 1980 57.48513 -63.75497 178.7252 -127.9356 242.9059 1981 57.50627 -63.73386 178.7464 -127.9145 242.9271 1982 57.51684 -63.72330 178.7570 -127.9040 242.9376 1983 57.52212 -63.71802 178.7623 -127.8987 242.9429 1984 57.52476 -63.71538 178.7649 -127.8960 242.9456 1985 57.52607 -63.71407 178.7662 -127.8947 242.9469 1986 57.52673 -63.71341 178.7669 -127.8941 242.9475 1987 57.52706 -63.71308 178.7672 -127.8937 242.9479 1988 57.52723 -63.71291 178.7674 -127.8936 242.9480 1989 57.52731 -63.71283 178.7674 -127.8935 242.9481 1990 57.52735 -63.71279 178.7675 -127.8934 242.9481 1991 57.52737 -63.71277 178.7675 -127.8934 242.9482 1992 57.52738 -63.71276 178.7675 -127.8934 242.9482 1993 57.52739 -63.71275 178.7675 -127.8934 242.9482 1994 57.52739 -63.71275 178.7675 -127.8934 242.9482 1995 57.52739 -63.71275 178.7675 -127.8934 242.9482 1996 57.52739 -63.71275 178.7675 -127.8934 242.9482 1997 57.52739 -63.71275 178.7675 -127.8934 242.9482 1998 57.52739 -63.71275 178.7675 -127.8934 242.9482 1999 57.52739 -63.71275 178.7675 -127.8934 242.9482 2000 57.52739 -63.71275 178.7675 -127.8934 242.9482

We can plot the original time series, and the forecasted values, by typing:

> plot.forecast(volcanodustseriesforecasts)

One worrying thing is that the model has predicted negative values for the volcanic dust veil index, but this variable can only have positive values! The reason is that the arima() and forecast.Arima() functions don’t know that the variable can only take positive values. Clearly, this is not a very desirable feature of our current predictive model.

Again, we should investigate whether the forecast errors seem to be correlated, and whether they are normally distributed with mean zero and constant variance. To check for correlations between successive forecast errors, we can make a correlogram and use the Ljung-Box test:

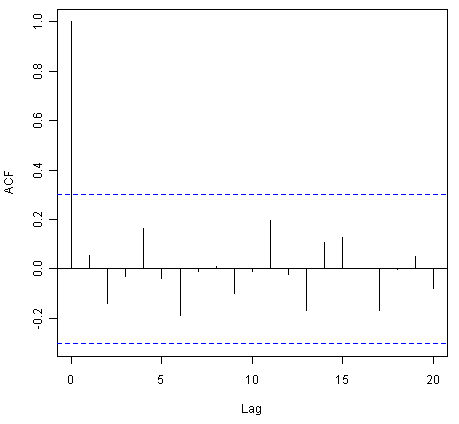

> acf(volcanodustseriesforecasts$residuals, lag.max=20) > Box.test(volcanodustseriesforecasts$residuals, lag=20, type="Ljung-Box") Box-Ljung test data: volcanodustseriesforecasts$residuals X-squared = 24.3642, df = 20, p-value = 0.2268

The correlogram shows that the sample autocorrelation at lag 20 exceeds the significance bounds. However, this is probably due to chance, since we would expect one out of 20 sample autocorrelations to exceed the 95% significance bounds. Furthermore, the p-value for the Ljung-Box test is 0.2, indicating that there is little evidence for non-zero autocorrelations in the forecast errors for lags 1-20.

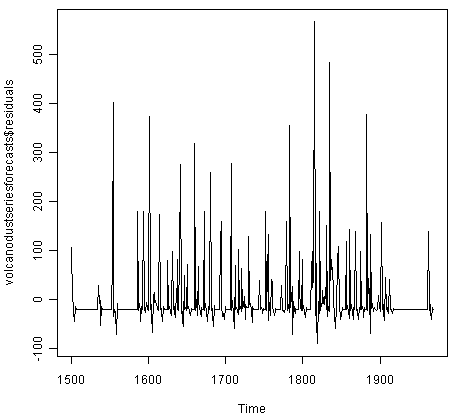

To check whether the forecast errors are normally distributed with mean zero and constant variance, we make a time plot of the forecast errors, and a histogram:

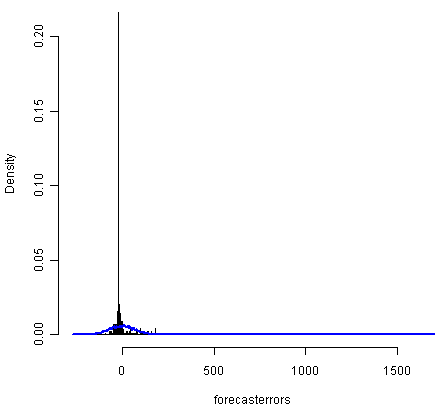

> plot.ts(volcanodustseriesforecasts$residuals) # make time plot of forecast errors > plotForecastErrors(volcanodustseriesforecasts$residuals) # make a histogram

The time plot of forecast errors shows that the forecast errors seem to have roughly constant variance over time. However, the time series of forecast errors seems to have a negative mean, rather than a zero mean. We can confirm this by calculating the mean forecast error, which turns out to be about -0.22:

> mean(volcanodustseriesforecasts$residuals) -0.2205417

The histogram of forecast errors (above) shows that although the mean value of the forecast errors is negative, the distribution of forecast errors is skewed to the right compared to a normal curve. Therefore, it seems that we cannot comfortably conclude that the forecast errors are normally distributed with mean zero and constant variance! Thus, it is likely that our ARIMA(2,0,0) model for the time series of volcanic dust veil index is not the best model that we could make, and could almost definitely be improved upon!

Links and Further Reading

Here are some links for further reading.

For a more in-depth introduction to R, a good online tutorial is available on the “Kickstarting R” website,cran.r-project.org/doc/contrib/Lemon-kickstart.

There is another nice (slightly more in-depth) tutorial to R available on the “Introduction to R” website,cran.r-project.org/doc/manuals/R-intro.html.

You can find a list of R packages for analysing time series data on the CRAN Time Series Task View webpage.

To learn about time series analysis, I would highly recommend the book “Time series” (product code M249/02) by the Open University, available from the Open University Shop.

There are two books available in the “Use R!” series on using R for time series analyses, the first is Introductory Time Series with R by Cowpertwait and Metcalfe, and the second is Analysis of Integrated and Cointegrated Time Series with R by Pfaff.

Acknowledgements

I am grateful to Professor Rob Hyndman, for kindly allowing me to use the time series data sets from his Time Series Data Library (TSDL) in the examples in this booklet.

Many of the examples in this booklet are inspired by examples in the excellent Open University book, “Time series” (product code M249/02), available from the Open University Shop.

Thank you to Ravi Aranke for bringing auto.arima() to my attention, and Maurice Omane-Adjepong for bringing unit root tests to my attention, and Christian Seubert for noticing a small bug in plotForecastErrors(). Thank you for other comments to Antoine Binard and Bill Johnston.

Contact

I will be grateful if you will send me (Avril Coghlan) corrections or suggestions for improvements to my email address alc@sanger.ac.uk

License

The content in this book is licensed under a Creative Commons Attribution 3.0 License.

'프로그램 > 데이터마이닝' 카테고리의 다른 글

| Big Data Analytics at Google Scale (0) | 2021.01.12 |

|---|---|

| 무료 데이터 시각화 및 분석 툴 정리표 (0) | 2021.01.11 |

| 리프트 차트(Analysis Services - 데이터 마이닝) (0) | 2021.01.10 |

| 빅데이터 시각화툴 정리 (0) | 2021.01.10 |

| R - 시계열 단순 예측 모형 (0) | 2021.01.10 |